Israel Housing Collapse?

- J.P. Katz

- May 7

- 5 min read

Updated: May 10

Real Unemployment soars to 16.6% in March 2026 with a 85,000 unit surplus

Israel’s Housing Disruption: The Hidden Economic Crisis Behind the Numbers

In early 2026, Israel’s economy appeared surprisingly resilient on paper. Headlines pointed to rising GDP, falling official unemployment, and continued economic growth despite war, inflation, and geopolitical uncertainty. But beneath those optimistic indicators, a very different reality was emerging for hundreds of thousands of Israelis.

According to data analyzed from the Israel Central Bureau of Statistics, a broader measure of labor displacement suggests that Israel may be facing one of the most significant employment disruptions in its modern history — with potentially massive consequences for the housing market, renters, homeowners, developers, and the broader middle class.

The warning signs are no longer theoretical.

The Official Unemployment Rate May Be Missing the Bigger Picture

Traditional unemployment statistics only count people actively searching for work within a recent period. That narrow definition excludes large groups of struggling workers:

People who gave up looking for work

Underemployed professionals earning far below their prior income

Workers furloughed indefinitely

Employees temporarily absent for “economic reasons”

These hidden categories now represent the real story of Israel’s labor market.

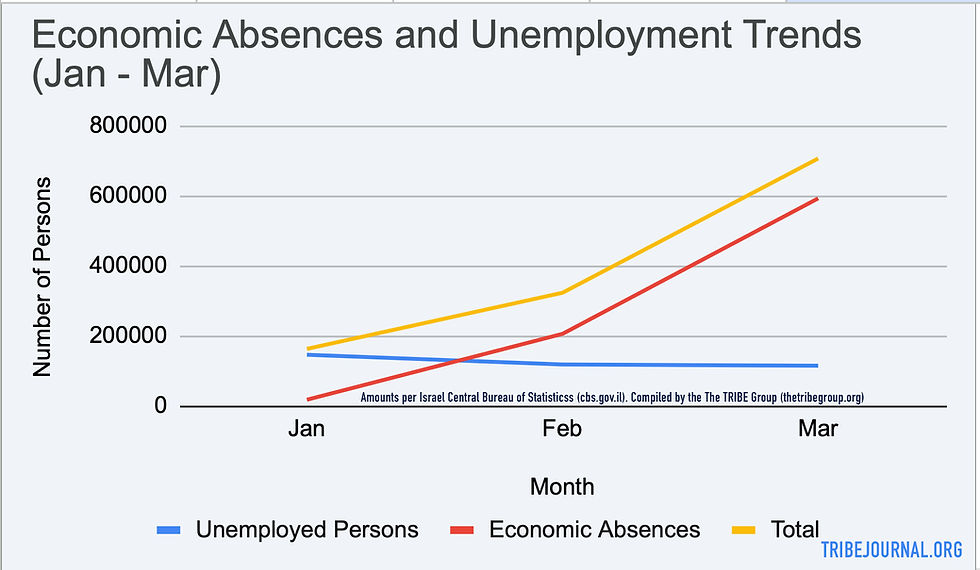

Official unemployment numbers looked relatively stable in the first quarter of 2026. In January, roughly 145,000 Israelis were officially unemployed. By March, that number had actually declined to around 114,000.

On the surface, that appears positive.

But another category exploded: employed persons temporarily absent from work due to economic reasons.

These are workers who technically still have jobs but were told not to come into work because employers could not pay them or lacked sufficient business activity. In many cases, these workers receive no salary despite remaining classified as employed.

According to The TRIBE Group’s analysis of CBS data, workers absent for economic reasons sound serious alarm bells with the following estimates:

January 2026: 16,000

February 2026: 205,000

March 2026: 592,000

Combined with official unemployment, the broader displacement figure reached approximately 705,000 Israelis by March — roughly 15.8% of the labor force. When discouraged workers and additional categories were included, the broader estimate climbed to about 16.6%, or roughly 747,000 people.

That scale of disruption dramatically changes how the economy looks from the ground level.

Why GDP and Employment Are No Longer Moving Together

One of the podcast’s central arguments is that traditional economic indicators may no longer accurately reflect the lived experience of workers.

Historically, economists expected a correlation between GDP growth and employment growth. When economies expanded, companies hired more people.

But artificial intelligence, robotics, and automation are beginning to weaken that relationship.

A company can now increase productivity and profits while reducing labor costs. GDP may rise even as workers lose income or employment stability.

This creates a dangerous illusion:

Stock markets can rise

Corporate profits can increase

National output can grow

While workers simultaneously experience economic deterioration

Israel may be entering this disconnect phase while other industries such as construction stall.

In that environment, headline unemployment figures become less meaningful than broader measures of labor displacement and financial insecurity.

The Housing Market Is Showing Signs of Stress

The employment disruption becomes even more significant when viewed alongside Israel’s housing market.

For years, Israel has faced a severe affordability crisis. Prices rose dramatically while wages lagged behind. Investors poured capital into real estate, encouraged by favorable tax treatment and long-standing assumptions that “housing in Israel always goes up.”

Now, however, several structural pressures appear to be converging.

More than 85,000 unsold housing units ARE sitting on the market — a large inventory surplus by Israeli standards. Many of these developments target higher-income buyers, while lower and middle-income households struggle to afford either ownership or rent.

At the same time:

Rent prices continue climbing

Mortgage burdens remain high

Developers face tightening financing conditions

Buyers increasingly depend on aggressive financing structures

One especially controversial mechanism discussed is the “10%/90%” financing model.

Under these arrangements:

Buyers place only 10% down initially

The remaining 90% is delayed until project completion

In some cases, mortgage payments are deferred for years after buyers move in

These structures helped fuel demand during the boom years. But they also created enormous vulnerability if employment conditions deteriorate before projects are completed.

If buyers lose jobs before final payments come due, they may default, lose deposits, or fail to qualify for mortgages altogether.

That creates risks not only for households but also for developers, lenders, and investors.

What Happens If Employment Weakness Deepens?

What happens to housing prices if large numbers of people can no longer afford rent or mortgages?

The answer could reshape Israel’s real estate market over the next several years.

Several possible scenarios are explored:

1. A Significant Housing Correction

Some analysts such as Haim Etkin predict a major market adjustment of 25–30% and the banks freezing accounts and adjusting the entire market.

Such a decline would erase much of the equity many buyers recently placed into properties. Buyers who entered projects with minimal down payments or showed inflated income to access additional financing could quickly find themselves underwater.

2. Inflation as a Pressure Release Valve

Another possibility is that policymakers attempt to soften the crisis through monetary expansion:

Lower interest rates

Easier credit

Increased liquidity

Currency depreciation

Inflation could theoretically reduce the real burden of debt over time, though at the cost of purchasing power and financial stability.

3. Government Intervention

Mortgage assistance, subsidies, or emergency housing support could emerge if defaults rise significantly.

But that introduces political and ethical questions:

Who receives assistance?

Who pays for it?

How much market intervention is sustainable?

The Structural Problem Behind Israeli Housing

Another uniquely Israeli dynamic is the government’s control over land supply.

Roughly 90% of land in Israel is state-controlled. Development decisions are therefore highly centralized through government agencies and planning authorities.

This gives policymakers and institutional bureaucracy enormous influence over:

Housing supply

Density approvals

Construction incentives

Stalling of newly approved cities

Affordability outcomes

Critics argue that current incentives disproportionately favor large-scale luxury or high-margin development rather than affordable housing solutions.

At the same time, decades of tax incentives encouraged investors to move capital into residential real estate, increasing competition for ordinary buyers.

The result has been a widening divide between asset owners and working households.

The Emerging “K-Shaped” Economy

Perhaps the most important concept to address is the “K-shaped economy.”

In a K-shaped recovery:

Wealthier asset owners continue rising upward

Lower and middle-income workers fall further behind

If employment instability worsens while housing costs remain elevated, that divide could intensify dramatically.

Renters may exhaust savings.Mortgage holders may struggle with payments.Developers may face stalled projects.Investors may encounter declining asset values.

Meanwhile, households and corporations with substantial capital reserves may gain even greater leverage over distressed markets.

A Crisis or a Transition?

This moment is not only a housing crisis but is part of a broader technological and economic transition.

Artificial intelligence and automation may eventually create enormous abundance and productivity. But the transition period could be deeply disruptive if labor markets, housing systems, and public policy fail to adapt quickly enough.

The underlying warning is clear:an economy can look healthy statistically while large portions of the population quietly experience financial collapse.

Whether Israel is entering a temporary correction or a deeper structural disruption remains uncertain. But the labor displacement numbers in March 2026 CBS data suggest that the warning lights are already flashing and the music may have stopped.

For policymakers, investors, homeowners, renters, and families considering aliyah, the coming months and years may require a far more cautious reading of the economy than official headlines alone provide.

Comments